The Art of Commerce: Part I

The Third Revolution

In this new 3-part series, our Chief Digital Officer Björn Köster and Chief Marketing Officer Hubert Eiter explore recent developments in the realm of online and offline retailing and dissect the implications for the consumer electronics industry with some exclusive expert insights.

Much has been said about the new retail revolution that experienced a major boost due to the pandemic. Digitalization is here to stay, but what exactly does that mean for stores? How can brands best adapt to the new retail normality? Will we still flock to the high streets to do our Christmas and Black Friday shopping? Or should brands, retailers and distributors go ahead and put all eggs into the e-commerce basket?

The end of retail as we know it?

According to a March 2021 social report in the Economist (The future of shopping), more than 16,000 stores shut and 183,000 retail jobs were lost in Britain in 2020, the most prominent victim being the Arcadia group with high-profile name like Topshop and Debenhams.

The toll in other parts of Europe or the US was not much better, with 2.4m jobs lost in March 2020 in the US alone. By January only about 2m jobs had been reinstated in retail; however, the Progressive Policy Institute think tank claims that industries related to e-commerce created 900,000 jobs more between the end of 2007 and the beginning of 2020 than those that were lost at brick and mortar stores.

Retail is truly a dominating factor of any modern economy. In the US alone, says the National Retail Federation, retailers are the largest private sector employers in America, engaging some 32m people. In the EU, about one in six workers have retail or wholesale jobs.

While the industry was really created in 16th-century England when craftsmen, who until then had made one-to-one trades with customers, set up first shops to sell other people’s goods, earning mark-ups. Retail saw a second big transformation during the industrial revolution, when mass produced goods entered the scene and economies of scale were the name of the game.

The third revolution was coined the “digital transformation” and is expected to really turn the existing model upside down. Instead of manufacturers and retailers being equal partners and dominating supplies, current successful models are much more geared towards consumers.

A Dance with Dragons

What this means can be seen in China with Pinduoduo (PDD), the country’s fastest growing internet stock, which rose by 330% in 2020, driving its market value to above $ 200bn.

With the help of PDD, consumers club together in groups to buy products in bulk. From vacuum cleaners to bananas. This reduces shipping and logistic costs for retailers, allows local producers and brands to reach a much larger audience and provides rock-bottom prices for consumers.

However, anyone that already sees the demise of the physical store might be wrong. According to the latest Euromonitor report on global retail, physical retail will remain the most important and biggest channel globally over the next five years with a share of 85% of today’s total and a dominant 77% expected in 2024, still.

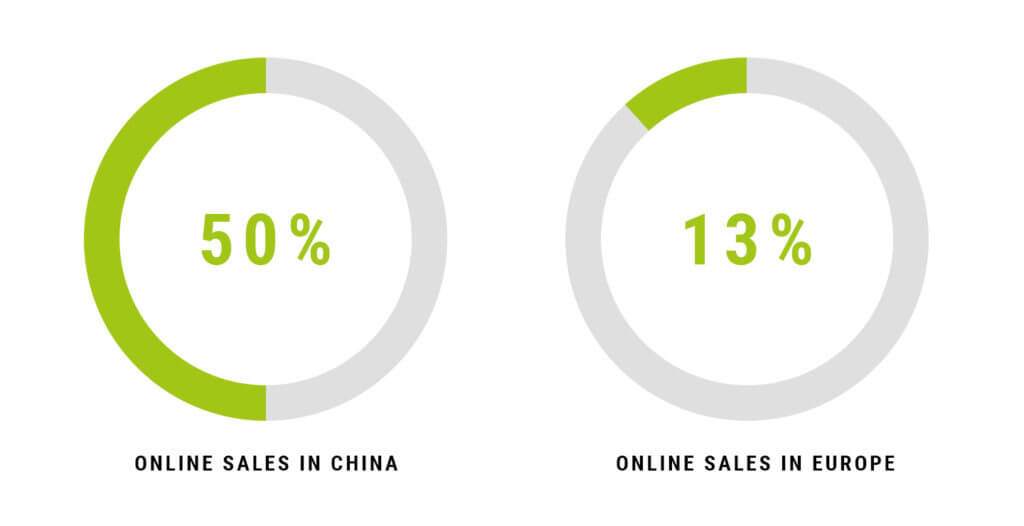

The leader in terms of online shopping is and will remain China. Online sales already make up 50% of total sales there, while most of Europe and the US are around 12-13% (Britain being the exception with close to 30% of the total). It feels natural for western retailers to now look east. According to a previous Economist article, e-commerce in China overtook America in 2013 and today is worth more than America and Europe combined.

But apart from its sheer size, Chinese e-commerce is also buzzing dynamic-wise. Online shopping platforms now blend payment, group deals, gaming, instant messaging and celebrity live-streams all in a single space. Western e-tailing resources seem outdated when compared to super-apps with a whole cornucopia of new services.

What is changing everywhere is the way data is being used to inform manufacturing. Nike and GoPro, for instance, for that matter, are a case in point with their decision to cut out a majority of wholesalers (including Amazon), which in turn led to a proliferation of the direct to consumer (DTC) model. Today 250m (!) people are in some sort of membership relationship, and Nike connects to them through a series of apps that provide services from free running guides all the way down to sneaker vending machines.

DTC now accounts for 40% of Nike’s revenues, and a big success factor in this game is the ultimate aim to replicate the “one-to-one” commerce that was so important for the start of the business, when running shoes were put on the feet of one runner at a time. The data-driven shopping upheaval is unstoppable. It will change the nature of stores, it will disrupt marketing, and it will lead to new forms of production – as it did for Nike when they increased their yoga wear output early on in the pandemic due to signs from their customer base.

Adding fuel to the fire – How the pandemic accelerates digitalization of retail

According to a recent DACH e-commerce report by Kantar Sifo & Nets Group, more than 96% of all Germans, Austrians and Swiss have acquired at least one service or product online in 2020. And it doesn’t appear to be some sort of pandemic peculiarity. The study indicates that one out of four plans to change their consumer behavior towards e-commerce.

These and similar kind of numbers these days are disruptively high, but they don’t necessarily signal the death of offline retail. Traditional retail stores do have a future, and you even see Amazon and other internet players develop their own brick and mortar networks. The question is how traditional shopping habits integrate into modern shopping environments. A number of trends will dominate the new normal in retail, and we are going to look at each of them in more detail:

- Social shopping

- Made to measure

- Conversational commerce

- Store formats

- Everything becomes shoppable

All these movements can be cross-referenced with the term “omnichannel”, which labels a world where online and offline merge and work seamlessly together. The trick is to make shops not just sales nodes but ways for shoppers to interact with the product and to experience the brands.

But before going into detail, let’s ask one of our main customers how they experienced the shift during the pandemic:

What is the biggest customer benefit of digitilization in retail?

No customer will ever complain about more choices, a better experience, a good price. Digital hasn’t fundamentally changed that, but it has enabled a lot of things on a whole new level. The selection alone is so much better today. In fashion retail, the stock used to be where you couldn’t use it in the end.

“Partial allocation” was a first step there. Now, through networking and omnichannel, demand can be much better matched to supply. Zalando connected retail not only allowed brick and mortar retailers to sell during the lock down, but also allowed customers to get their sizes delivered faster.

What is THE most important reason to still operate physical stores?

The physical and social experience remains an important factor. After all, Apple demonstrated this years ago. Omnichannel is the future, though. You only have to look at China, for example, to see how Alibaba hippo stores are blurring the boundaries.

What was the biggest innovation in ecommerce in the last 12 months at Zalando?

The acceleration of the channel switch was very special from my point of view. Customers and suppliers have turned to digital channels with an unprecedented openness. At the same time, we were able to launch a number of innovations at Zalando. For end-consumers, for example, our “plus program” with benefits along the customer journey (from shipments to special offers) and for our partners, for example, connected retail and Zalando fulfillment were further expanded.

If you liked this article, check out part 2, and don’t miss out on our previous miniseries. Our Vice President Klaus Trapl examines the success formula of challenger brands and explains why they’re so powerful: